September 28, 2020

During the FOMC’s September press conference, Fed Head Jerome Powell managed to communicate three big lies in the space of an hour. The fact that bile spews from the mouth of a central banker isn’t all so surprising. However, having to suffer through three humongous untruths in about an hour was remarkable—even for the Fed.

Mr. Powell was asked by a reporter why the US economy needed an inflation rate of 2% to function properly, and why Americans would now need to have their savings depreciated to some degree above 2% for an extended duration.

So here was lie number one: Powell’s specious reasoning behind wanting higher inflation is that it would engender higher interest rates, which would then allow the Fed room to lower rates whenever a recession inevitably arrives. This means the Fed is oblivious to another zero figure to match its 0% return forced upon savers. There’s zero evidence, either historically or logically, that an economy needs a sustainable 2% + rate of inflation on the Core PCE Price Index to function properly.

Regardless… let’s leave aside the insanity behind wanting to pursue inflation just so there is room to lower rates once the recession arrives—a recession that is always facilitated by its monetary largess in the first place. It is far from the truth behind the Fed’s real motivation. The actual purpose behind its stated goal to create a condition of permanently rising inflation is to pump up asset prices into a perpetually-expanding bubble. This condition has now become necessary in order to ensure Wall Street and banks get bailed out of what would otherwise be a condition of insolvency.

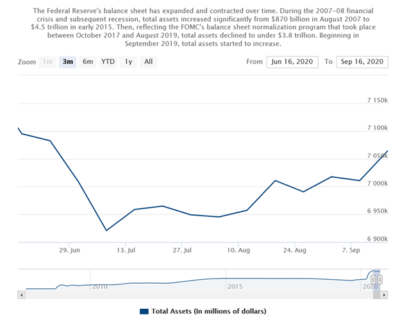

The second lie was that the Fed would continue to buy Treasuries and MBS equal to a pace of at least $120 billion each month. However, this is clearly not been the truth—at least not of late. If Powell was indeed adding $120 billion to his balance sheet each month, it would have increased by $360 billion, instead of being static over the past three months.

As to why the Fed Head would mislead regarding the recent pace of increase in asset purchases is unclear. What is very clear, however, is that he will not reach his newly-raised inflation target by simply claiming he is monetizing debt at a record pace. The balance sheet did skyrocket from March thru June by over $3 trillion. But over the past quarter of a year, the balance sheet has gone nowhere. Indeed, what the Fed really needs is the unholy cooperation of Treasury with a Universal Basic Income guarantee to get consumer inflation to really pick up the pace. Thankfully, that is not happening yet.

The third, and perhaps biggest lie, was that the Fed’s massive increase in its balance sheet, which did occur over the past dozen years, did not lead to any asset bubbles. Powell was asked directly in the press conference if the Fed’s QE programs and zero interest rate policy (ZIRP) put into place the dangerous conditions of asset price inflation and financial instability. His response was that the Fed’s seven years of ZIRP and $6.2 trillion in QE was “notable for the lack of the emergence of some sort of a financial bubble.” He continued, “I don’t know that the connection between asset purchases and financial stability is a particularly tight one.” Really?

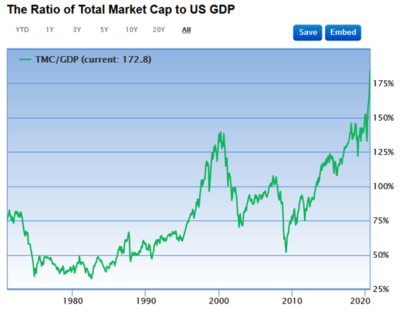

The S&P 500 now trades at a trailing price to earnings ratio of 27.2, which is closing in on double its historical average of 16, according to data from Refinitiv. Not only this, but the all-important Total Market Cap to GDP Ratio has now surged to an incredible 175%, which is far above its historical average and even dwarfs the previous high of 145% set in March of 2000 just before the NASDAQ lost 83% of its value.

In reality, Powell knows his statements are a fallacy because the overvalued and unstable stock market fell apart in the late summer of 2018 when the Fed was undergoing a half-hearted attempt to normalize interest rates and pare down the size of its balance sheet by just a few hundred billion dollars. This is, of course, after blowing it up by multiple trillions over the past dozen years.

But it’s not just the stock market that is in a massive bubble. The economy is also in one as well. Data put out by the Federal Reserve show that total non-financial debt in the US increased at an annualized rate of 25.27% in Q2, –shattering all known records! That debt explosion was primarily due to a 58.86% surge in Federal Government debt and a 14.02% jump in business debt. And no, this humongous debt binge wasn’t even close to being commensurate with a rise in our phony GDP. Business debt is now 83% of GDP, whereas it was just about 60% at the peak of the NASDAQ bubble. Government debt was 40% in the year 2000, but now it is well above 100%.

Of course, record-low borrowing costs (provided by the Fed) compels businesses to take on more debt and enables the Treasury to also issue bonds at the central bank’s falsified interest rates. Mr. Powell appears to be ignorant of these conditions. And if the Fed remains blissfully unaware, how then can it assume responsibility?

Nevertheless, the Fed’s unstable economy and stock market bubble was on full display in the past few weeks. Tech stocks of the FAANG variety, which Wall Street has overcrowded into with unprecedented measure, were obliterated. Take AAPL, for example; it crashed by nearly 20% from the start of September. The mighty Google (Alphabet) plunged by 18%. And, even the S&P 500 hit an air pocket that saw a 3-day plunge of nearly 8% at the start of this month.

Hence, the value of having an actively managed strategy that is built on a solid model was again illustrated.

It is abundantly clear that the economy and markets are in massive bubbles. While the high-frequency components of the Inflation/Deflation and Economic Cycle model are not flashing red at this time (it’s just amber at this moment), our leading components do indicate we may be heading in that direction. The pending election chaos, along with a massive fiscal and monetary cliff, could be paving the way to even greater volatility. If you are still invested in a passively managed and long-only portfolio, the time to act is now.

Michael Pento is the President and Founder of Pento Portfolio Strategies, produces the weekly podcast called, “The Mid-week Reality Check” and Author of the book “The Coming Bond Market Collapse.”