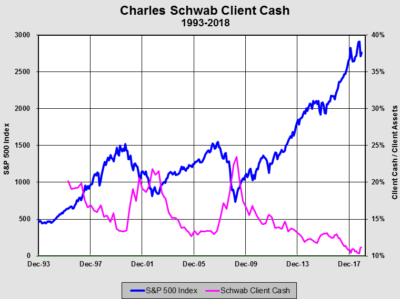

It’s been a wild ride on Wall Street lately. Major averages had hit their highs in late September. But if this sell-off continues, it will be Wall Street’s worst year since the financial crisis and the worst December since the Great Depression! This should have been enough to shake investor confidence. But judging from the data in the chart below, compiled by my friend Kevin Duffy of Bearing Asset Management and using data from Charles Schwab, we see that investors on both the retail and institutional level have a near-record low level of cash. They are anything but scared of this market.

This data was compiled on November 30, 2018, when cash levels registered just 11.2%. That was not up much from the low reading of 10.3% held on September 30th. The retail investors is, relatively speaking, all in.

And, analysts aren’t pulling in their horns either.

According to FactSet: Overall, there are 11,136 ratings on stocks in the S&P 500. Of these ratings from Wall Street analysts, 53.9% are Buy ratings, 40.8% are Hold, and just 5.3% are Sell ratings. Yet, with the mounting weight of evidence in favor of a sharp slowdown in global growth, it has not dissuaded analysts from still having ebullient forecast for earnings growth next year. Analysts are projecting S&P 500 EPS estimates for the Calendar year 2019, according to FactSet, to grow at 8.3% with revenue growth of 5.5%.

The global economy is showing signs of cracking now that QE has gone from $180 billion per month in 2017, to a negative number in 2019. That has sent the Emerging Markets into chaos and help lead European and Japanese economies into contraction.

And now China, which has been responsible for 1/3rd of global growth coming out of the Great Recession, is entering into a recession. Of course, having the government force an increase of debt to the tune of 2,000 percent since the year 2000 guarantees a crash of historic proportions. In fact, the government in Beijing is so concerned about the current debacle that it has banned the gathering of private economic data.

According to the South China Morning Post, China’s central government has ordered authorities in the Guangdong province – China’s main manufacturing hub–to stop producing a regional purchasing managers’ index. This means the province will not release the purchasing managers’ index (PMI) data for both October or November. Instead, all future purchasing managers’ indexes will be produced in-house by the National Bureau of Statistics.

It is evident that Beijing is trying to suppress the dissemination of economic data because its economy is growing at a much slower rate than what the communist party will admit to…that is, if it is growing at all. This is hindering its position in negotiations with the United States in the trade war. And it also reiterates the complete lack of transparency in the Chinese markets and the desire on the part of the Chinese government to keep the world in the dark about the true state of its economy.

Perhaps December’s continued debacle in global markets and economies was enough to begin pushing U.S. investors toward the exit–we will monitor this dynamic closely. However, history shows that it is a multi-month process to move investors’ psyche from euphoria to panic. This dynamic is still in its infancy.

Michael Pento is the President and Founder of Pento Portfolio Strategies, produces the weekly podcast called, “The Mid-week Reality Check” and Author of the book “The Coming Bond Market Collapse.”